Tax Planning Strategies for High-Income Earners

Paying taxes may be inevitable, but there are strategies high-income earners can employ to reduce their tax burden and potentially keep more of their income. If you find yourself in the higher tax brackets—or you’ve encountered unexpected tax liabilities—it may be worthwhile to explore available tax planning strategies. From understanding your tax bracket to maximizing deductions and retirement plan contributions, a proactive approach can help you retain more of your hard-earned money.

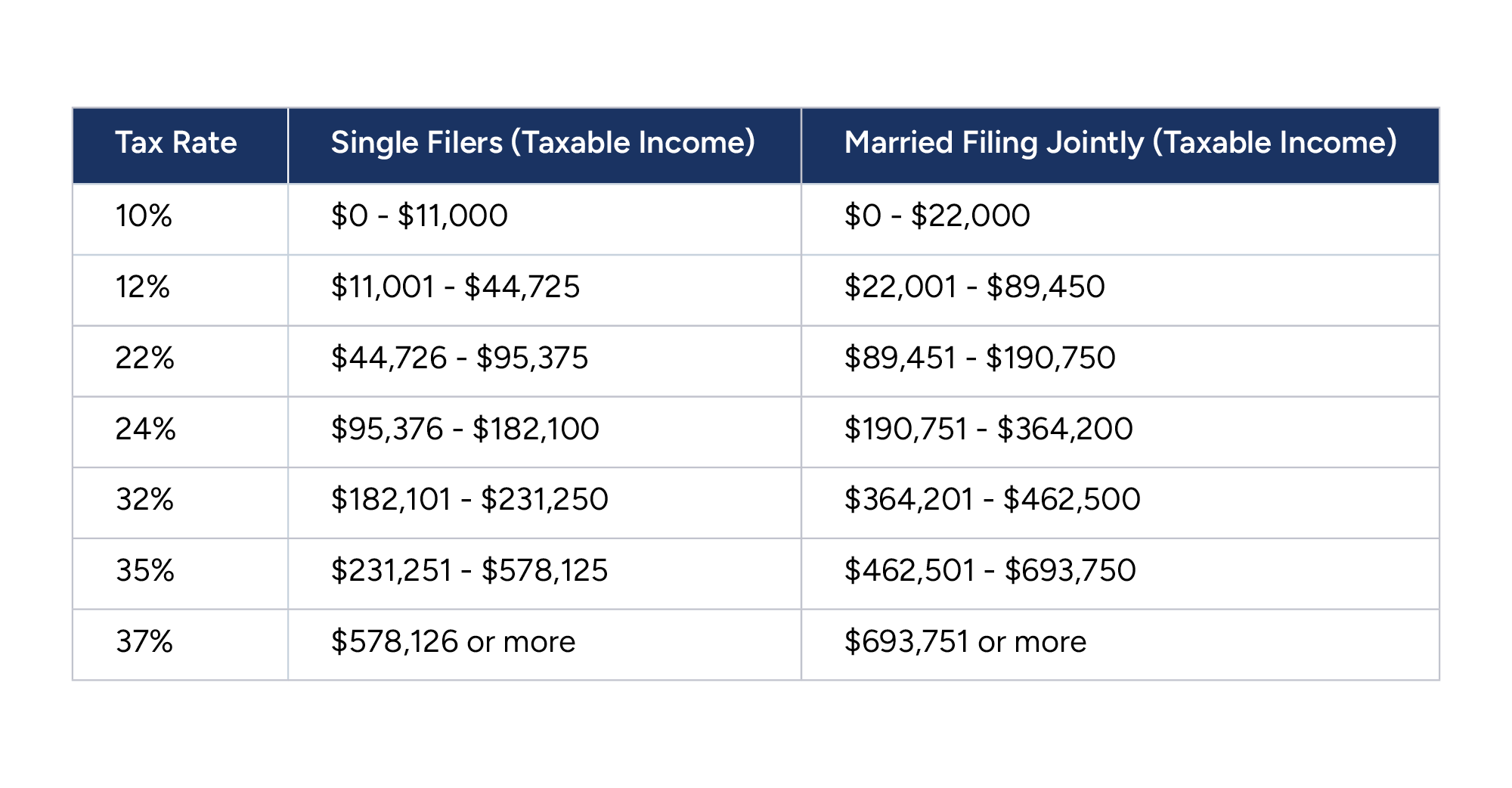

Understanding the Federal Brackets

The U.S. federal income tax system follows a progressive structure, meaning the rate increases as taxable income grows. Below are the federal tax brackets for the 2025 tax year for both single filers and married couples filing jointly. Keep in mind that these brackets and rates can change, and certain deductions or credits may alter your effective bracket.

Deductions & Credits

Standard Deduction vs. Itemizing

If you have sizable expenses—such as mortgage interest, charitable donations, or high medical costs—itemizing may offer a larger total deduction compared to taking the standard deduction. For high-income earners, weighing these options carefully can make a noticeable impact on overall tax liability.

Charitable Contributions

Donations to qualified charities can reduce your taxable income. If you have appreciated assets, consider donating them instead of cash. This approach can maximize your deduction while also bypassing capital gains taxes on the appreciation. Additionally, utilizing a Donor Advised Fund (DAF) allows you to make a charitable contribution, receive an immediate tax deduction, and recommend grants to charities over time. A DAF can be an effective strategy for managing charitable giving while optimizing tax benefits.

Business Deductions

Business owners and self-employed individuals can claim deductions for a variety of expenses, including home office costs, travel, and equipment purchases. Accurate record-keeping is essential to substantiate these deductions and withstand potential IRS scrutiny.

Retirement Contributions

Maximizing 401(k) and IRA Contributions

For 2025, contribution limits for 401(k) plans and IRAs have risen, which is especially beneficial for high-income earners looking to defer more income. By leveraging different retirement plan options, business owners can significantly increase their contributions while also benefiting from potential tax deductions.

- 401(k): Individuals under 50 can contribute up to $23,500, while those 50 or older can make an additional catch-up contribution of $7,500. For individuals aged 60 to 63, the catch-up contribution limit is increased to $11,250.

- Profit-sharing contributions allow employers to contribute discretionary amounts to employee (including their own) retirement accounts, potentially increasing total contributions up to the annual defined contribution plan limit of $70,000 (or $77,500 with catch-up). A New Comparability Profit-Sharing Plan is an advanced strategy that enables business owners to allocate higher contributions to specific groups—such as key employees or owners—while maintaining compliance with nondiscrimination rules. This method can be particularly beneficial for business owners looking to maximize their own retirement savings while still providing benefits to employees.

- SEP & Solo 401(k) Plans: For self-employed individuals and small business owners, SEP IRAs and Solo 401(k)s offer opportunities to contribute up to 25% of compensation, up to the maximum limit. These plans provide flexibility in high-income years while reducing taxable income.

- IRAs (Traditional and Roth): Individuals under 50 can contribute up to $7,000, while those 50 or older can make an additional catch-up contribution of $1,000. However, the ability to deduct contributions or directly contribute to a Roth can phase out at higher income levels.

Backdoor Roth IRA

If your income exceeds the direct contribution limits for a Roth IRA, the “backdoor” strategy may be an option. It involves making a non-deductible contribution to a traditional IRA and then converting those funds to a Roth IRA. Keep in mind the pro-rata rule, which can complicate your taxes if you hold other traditional IRA funds.

Other Key Tax Planning Strategies

- Income Timing: If your compensation structure allows, consider deferring bonuses or other income to a year when you anticipate a lower tax bracket.

- Capital Gains Management: Use tax-loss harvesting to offset realized capital gains. Also, aim to hold assets for over a year to benefit from lower long-term capital gains rates.

- HSAs and FSAs: Contributing to Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) can reduce taxable income while covering qualified healthcare expenses.

- Estate Planning: Strategies like trusts and lifetime gifting can help very high-income earners reduce future estate tax liabilities and transfer wealth more efficiently.

- Business Entity Selection: If you’re a business owner, your choice of entity (LLC, S-Corp, etc.) can greatly influence how your income is taxed.

Conclusion

High-income earners face distinct challenges when it comes to tax planning. By understanding your tax bracket, maximizing deductions, and strategically leveraging retirement accounts, you can significantly reduce your tax burden. Additionally, working with professional advisors can help ensure your approach is tailored to your individual financial circumstances—and that you’re prepared to adapt as tax laws change.

If you’d like to learn more about these tax planning strategies, schedule a call with one of our advisors at RW Wealth. A little planning now can pay off substantially in the long run.

Important Disclosure Information

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by RW Wealth (“RW”), or any non-investment-related content, made reference to directly or indirectly in this commentary) will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer reflect current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from RW. Please remember to contact RW, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing, evaluating, or revising our previous recommendations and/or services—or if you would like to impose, add, or modify any reasonable restrictions to our wealth management services.

RW is not a law firm and no portion of the commentary content should be construed as legal advice. A copy of RW’s current written firm brochure, which discusses our advisory services and fees, remains available upon request.